Irrevocable Trust Loans for California Real Estate

3 Reasons Beneficiaries Borrow

Irrevocable Trust Loan Request

An associate will contact you to review the loan scenario and provide a quote.

Irrevocable Trust Loans: 3 Reasons Beneficiaries Borrow

Irrevocable trust loans allow successor trustees and beneficiaries who have recently inherited real estate to borrow against the trust-owned property. Loans for irrevocable trusts are available but only from specialized irrevocable trust loan lenders. Lending to an irrevocable trust is typically not possible from banks or other institutional lenders.

Irrevocable trust loans to beneficiaries and trustees only provide short-term financing against trust-owned real estate. The irrevocable trust loan is essentially a home equity loan against the inherited real estate.

For trust beneficiaries

Need cash from an irrevocable trust before it settles?

Beneficiary buyouts, borrower for trust expenses, and get Prop 19 benefits with trust-secured loans, funded directly often within days.

- 45 years of lending experience

- $1B+ funded

- 5.0 star Google rating

- Direct California lender

3 Reasons Beneficiaries Borrow Against an Irrevocable Trust

Irrevocable trust lenders typically provide loans to trustees and beneficiaries for the following three reasons.

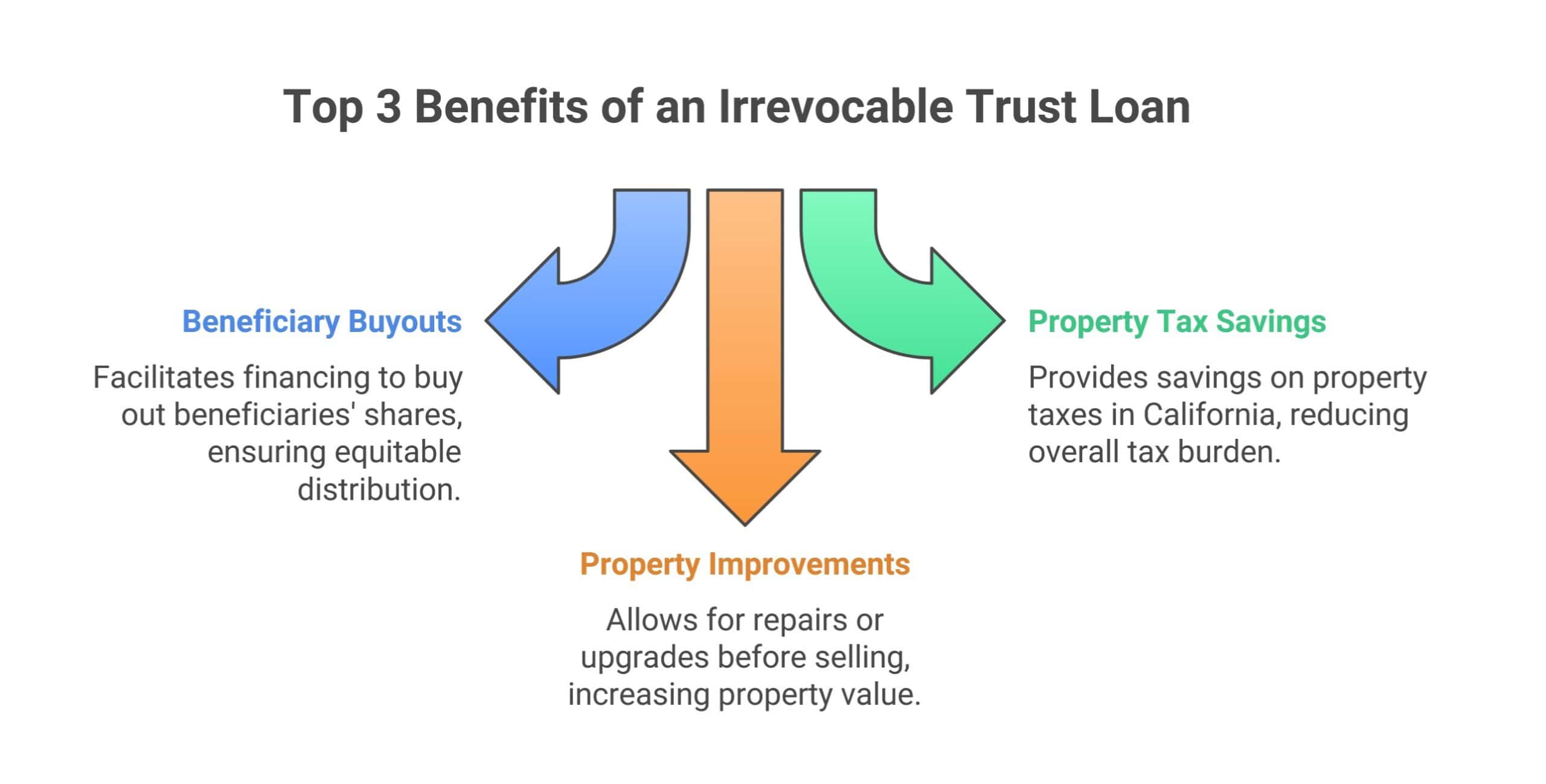

- Borrowing cash to pay for the trust’s expenses

- Buying out other beneficiaries to keep the property (trust equalization loan)

- Avoiding a property tax reassessment with Prop 19 or 58 (California)

1. Borrowing cash to pay for the trust’s expenses

A living or family trust becomes an irrevocable trust when the original trustees have passed. Once the original trustees have passed, beneficiaries and successor trustees need to ensure the financial expenses of the trust are being paid. Various expenses must be paid such as property taxes, mortgage payments, property maintenance and repairs and legal fees. Borrowing against the trust’s assets to cover expenses is a faster and easier option than selling trust assets. Mortgage loans to irrevocable trusts can be funded in as few as 5-7 days.

A successor trustee can encumber real estate assets owned by the irrevocable trust in order to raise the needed funds (if allowed by the trust documents). Irrevocable trust lenders need to review the trust documents as well as any amendments made to the trust.

2. Buying out other beneficiaries (siblings) to keep the property

Siblings and beneficiaries of an irrevocable trust often face the challenge of dividing trust-owned real estate assets. One sibling may want to sell the property and receive cash while another sibling may want to keep the property. If the trust doesn’t have enough assets to evenly split things between the siblings an irrevocable trust loan can help.

If the trust-owned real estate has sufficient equity, the sibling who wants to keep the property can use an irrevocable trust loan to borrow against the property. The loan proceeds from the irrevocable trust loan can then be used to buy out the other sibling(s). Irrevocable trust mortgage financing will be required to assist with the distribution of the real estate asset.

Conventional lenders such as banks and credit unions cannot typically provide an irrevocable trust mortgage as the sibling’s name is not yet on the title of the property.

An irrevocable trust loan lender is able to provide the loan directly to the trust with the loan proceeds going directly to the trust’s bank account. A deed of trust with a note is recorded against the real estate just like a traditional mortgage. The funds then be distributed to the siblings who are being paid in exchange for their interest in the real estate. Once the siblings have been paid, the title of the property can be transferred from the name of the trust to the name of the sibling who is keeping the property.

When the property title is transferred into the name of the sibling, they can then refinance the irrevocable trust loan into a long-term loan from a conventional lender.

3. Avoiding a property tax reassessment with Prop 19 or Prop 58

Another reason beneficiaries obtain an irrevocable trust loan is so they can file for Proposition 19 or 58 (California) and avoid a property tax reassessment. Real estate owned by trusts have often been in the family for decades. Properties in California that have been owned for a long period of time typically have a very low tax assessment relative to their current value due to Proposition 13. Prop 13 limits the annual increase on the existing property tax assessment value.

Prop 19 allows beneficiaries to prevent a property tax reassessment for transfers of real estate from the trust into the name of the beneficiary. Preventing a property tax reassessment can save thousands of dollars each year in property taxes.

To qualify for Prop 19 and obtain a reassessment exclusion from the county, the transfer of real estate must be directly from parent (trust) to child (beneficiary).

A beneficiary may have cash in their personal bank account they could use to pay off their siblings in exchange for sibling’s interest in the real estate. This transaction would not qualify for Prop 19 as it would be seen as a sibling to sibling to transfer since cash is being paid by one sibling to another. Sibling to sibling transfers do not qualify for Prop 19. A “3rd party loan” would be required to allow the trust to borrow against its own assets and obtain the necessary liquidity and equalize the distribution of the assets. Now that Proposition 19 has passed in California, beneficiaries will need to obtain a Prop 19 loan and comply with the new requirements to avoid a property tax reassessment.

As discussed previously, irrevocable trust loan proceeds go directly to the trust. The trust then distributes the funds to the beneficiary who is being paid off. Once the bought-out beneficiaries no longer have an interest in the property, title can be transferred from the trust to the beneficiary who will keep the property. This will qualify as a parent to child transfer. Now that the title has been transferred into the name of the beneficiary, the beneficiary can pay off the irrevocable trust loan with cash or refinance with a bank loan.

READ MORE: Understanding Irrevocable Trust Loans

*Consult an attorney or a tax professional to ensure the transfer is handled correctly in order to take advantage of Prop 58 or Prop 19.

How to Get an Irrevocable Trust Loan in California

Obtaining a loan for an irrevocable trust can be an excellent solution for beneficiaries who need to buy out siblings, preserve property tax benefits under Proposition 19 or settle financial obligations of the trust during a distribution. Below is a step-by-step guide to how the process works. Also see our Irrevocable Trust Loan Guide infographic.

Step 1: Review the Trust Documents

The first step is to determine whether the trust allows for borrowing. Trusts typically allow for the successor trustee to take out a loan against the trust’s assets as long as it is in the best interest of the trust and beneficiaries.

Step 2: Confirm Trustee Authority

Only the acting successor trustee(s) has the authority to borrow money on behalf of the trust. If you’re a beneficiary who is seeking a loan, you’ll need the cooperation of the successor trustee to initiate the loan application and sign the loan disclosures and documents.

Step 3: Determine the Purpose of the Loan

Irrevocable trust loans are commonly used to:

-

Equalize an inheritance (buyout siblings/beneficiaries)

-

Prevent a property tax reassessment under Prop 19 by transferring property to a child as a primary residence

-

Pay off debts, taxes, or expenses of the trust

- Borrow funds to make repairs and improvements to the trust property prior to selling

Clarifying the purpose of the trust loan helps determine the proper loan structure.

Step 4: Determine the Value of the Property

The trustee and beneficiaries may obtain an appraisal or Broker Price Opinion (BPO) to establish the current market value of the property. This determines the maximum loan amount available based on the trust’s equity. It’s important that the beneficiaries agree on the value of the property prior to moving forward with the loan.

Step 5: Apply for the Loan

Submit the loan application forms, trust documents and trustee information to a specialized irrevocable trust loan lender like North Coast Financial. We will evaluate the loan scenario, property, verify trustee authority and provide preliminary loan terms.

Step 6: Loan Approval & Funding

After reviewing all required documents, we’ll finalize the loan terms. Once approved, the initial loan disclosures and documents will be prepared and signed by the successor trustee. When the trust loan escrow closes, the loan funds are disbursed directly to the trust’s bank account. From approval to funding, the process generally takes 5–10 days.

Step 7: Use Loan Proceeds

The loan proceeds can be used to buy out other beneficiaries, settle debt obligations, improve the property or preserve a low property tax base for an inheriting child (Prop 19). These funds are secured by the trust’s real estate, and repayment terms are typically short-term (up to 12-24 months).

Need Help? Contact North Coast Financial

North Coast Financial specializes in California irrevocable trust loans and can guide you through every step of the process. Contact us today to discuss your situation and receive a free consultation.

5-Star Reviews from our Trust Loan Clients

Trust, Probate and Estate Loans Funded by North Coast Financial

Recent Deal – San Pedro Irrevocable Trust Loan

San Pedro Irrevocable Trust Loan North Coast Financial provided a $405,000 irrevocable trust loan in San Pedro, California (Los Angeles). A trust beneficiary buyout loan was needed to borrow against trust-owned real estate and also prevent a property tax reassessment. The trust loan was made directly to the trust and secured by the real estate. The loan proceeds went directly to the trust's bank account and were later distributed to the other beneficiaries. Once the real estate [...]

Recent Deal – Daly City Irrevocable Trust Loan

Daly City Irrevocable Trust Loan North Coast Financial provided a $815,000 irrevocable trust loan in Daly City, California (San Mateo County). A beneficiary buyout loan was needed in order to equalize the distribution of the trust's assets among three beneficiaries. One beneficiary wanted to keep the property while the other two wanted their inheritance in cash. North Coast Financial made a loan directly to the irrevocable trust which allowed the beneficiary to apply for Prop 19 with [...]

Recent Deal – San Diego Trust Loan

San Diego Trust Loan North Coast Financial financed a $515,000 trust loan in San Diego, California. One of the beneficiaries needed a sibling buyout loan in order to keep the property and pay out the other beneficiaries. The beneficiary needed a 3rd party irrevocable trust loan to apply for Prop 19 and help prevent a property tax reassessment. A single family residence owned by an irrevocable trust was used as collateral for the loan. The loan to [...]

Recent Deal – Sacramento Trust Loan

Sacramento Trust Loan North Coast Financial provided financing for a $515,000 trust loan in Sacramento, California. An irrevocable trust loan was needed to allow one beneficiary to buyout the other beneficiary and maintain ownership of the property. A 3rd party loan was needed so that the beneficiary could apply for Prop 19 and prevent property taxes from increasing.The loan was secured by a single family residence owned by the irrevocable trust. The loan to value was approximately [...]

Can a Trustee Take Out a Home Equity Loan on a Property That is in a Trust?

Yes, a trustee can take out a home equity loan on a property that is in a trust (including irrevocable trusts). The trust-owned real estate must have sufficient equity to borrow against and the trust documents must not prohibit the successor trustee(s) from borrowing against the real estate. The successor trustee must apply for and sign the loan disclosures and documents on behalf of the irrevocable trust. Can a trust take out a home equity loan?

A home equity loan requires the borrower (trust) to accept the full amount of the loan upfront. A line of credit against the real estate, commonly known as a home equity line of credit (HELOC), is typically not available from irrevocable trust loan lenders.

Using a Trust as Collateral for a Loan

Using a trust as collateral for a loan allows the trustee to quickly borrow against trust-owned real estate to provide the irrevocable trust with short-term liquidity. The real estate being used as collateral for the loan must have sufficient equity relative to the requested loan amount. Using a trust as collateral for a loan can be an excellent short-term option when needed to help equalize a trust distribution between beneficiaries or borrowing to fix up and sell a trust-owned property.

The risks of using a trust as collateral for a loan should be minimal as the trustee will need to have a reasonable plan and exit strategy in order to repay the short-term irrevocable trust loan. Common exit strategies include selling the property, paying the loan off with cash or refinancing the trust loan into a long-term traditional loan once the property is transferred out of the irrevocable trust and into an individual’s name.

Irrevocable Trust Loan Lenders

Irrevocable trust loan lenders provide short-term financing directly to an irrevocable trust. An irrevocable trust loan lender is usually a private money lender, which means the source of funds for the irrevocable trust mortgage is private investors as opposed to large banking institutions. Irrevocable trust mortgage financing is typically available for up to 3 years while most loans are written for 12 months and paid off much earlier.

An irrevocable trust lender is not able to provide a long-term 30-year irrevocable trust mortgage. If the property needs to stay within the irrevocable trust it will be difficult or impossible to obtain irrevocable trust mortgage refinancing. If the property is going to be transferred out of the trust and into an individual’s name, an irrevocable trust loan lender will be able to help. Once the property transfers out of the trust, the individual can refinance the irrevocable trust mortgage with a long-term conventional loan.

Irrevocable Trust Mortgage Refinancing

Irrevocable trust mortgage refinancing from specialized irrevocable trust lenders provides the successor trustee and beneficiaries with fast and easy financing to help distribute assets of the trust and equalize the distribution. Irrevocable trust mortgages can be funded within 5-7 days as long as there are not any issues with title or other delays that must be resolved prior to funding the loan. Traditional mortgages as well as reverse mortgages against the trust-owned property can be refinanced by the irrevocable trust mortgage.

The irrevocable trust mortgage is only intended to be a short-term loan to assist with the trust distribution. Once the property title has transferred out of the trust and into the name of the beneficiary that will keep the property, the beneficiary will be able to contact a conventional lender and start the process to refinance the irrevocable trust mortgage into a long-term traditional loan.

Related: Can a Beneficiary Borrow Money from a Trust?

Can an Irrevocable Trust Borrow Money from a Bank?

An irrevocable trust cannot borrow money from a bank or other traditional lenders in most situations. An irrevocable trust can obtain short-term financing from specialized irrevocable trust loan lenders if the successor trustee of the trust has a reasonable exit strategy for the loan. The most common exit strategies are transferring the property out of the trust and into a beneficiary’s name and then refinancing or selling the property in the near future. Lending against real estate within irrevocable trusts is typically too complex for banks to consider.

Why Might a Bank not Lend Money to an Irrevocable Trust?

Banks typically do not lend money to an irrevocable trust for various reasons. In many irrevocable trust loan request situations, the original trustor of the trust has passed and a new successor trustee would be applying as the borrower on behalf of the trust. This is an outside the box scenario for a conventional lender in which they would likely require that the real estate is transferred out of the irrevocable trust prior to providing trust financing.

A bank or conventional lender that lends to irrevocable trust may not be able to sell this loan on the secondary mortgage market which would prevent them being able to provide the loan to begin with.

Some attorneys advise clients to put real estate assets directly into an irrevocable trust as opposed to taking title in a living, revocable or inter vivos trust. Placing the real estate into an irrevocable trust is supposed to offer additional asset protection to the owner of the property but unfortunately this drastically reduces the types of financing available for the real estate.

Refinance Reverse Mortgage in Irrevocable Trust

Beneficiaries of an irrevocable trust may find themselves in a situation where an inherited property has a reverse mortgage. Reverse mortgage companies have a bad reputation for being aggressive and threatening foreclosure once the original trustee has passed. If the beneficiary wants to keep the property they will not be able refinance the reverse mortgage with a conventional lender because the property is in an irrevocable trust.

Unless the beneficiary has cash, they will need to refinance the reverse mortgage with an irrevocable trust loan lender. Refinancing the reverse mortgage will stop the harassment from the reverse mortgage company. This will give the beneficiary time to transfer the property into their name and then obtain a long-term conventional loan.

Probate & Estate Loans

Irrevocable trust loan lenders generally provide other types of inheritance loans such as probate and estate loans. Probate and estate loans are also secured against inherited real estate assets. The process is similar to trust loans. The estate loan is made to the estate directly and real estate is used to secure the loan. Estate loans are commonly used for the same reasons as trust loans. An estate loan to buy out siblings is one of the most popular reasons an estate loan is requested.

The information provided herein is for educational purposes only. North Coast Financial is not providing any legal, tax or financial advice.

Trust Loans Program

Need more information about trust loans? Click the button to learn more or Contact Us.

Irrevocable Trust Loan Frequently Asked Questions

Below are some of the most common frequently asked questions about irrevocable trust loans. See our Understanding irrevocable trust loans page for additional FAQs.

Can an irrevocable trust get a loan?

An irrevocable trust can receive a loan if the trust owns real estate with sufficient equity to borrow against. The trust documents must allow for the successor trustee or beneficiary to borrow against the trust-owned real estate. The loan would be made directly to the trust with the trust being the borrower.

Can an irrevocable trust guarantee a loan?

An irrevocable trust cannot guarantee a loan for which it is the borrower. The irrevocable trust can allow for a loan to be secured by trust-owned real estate assets but this isn’t considered a guarantee. A borrower is not able to guarantee their own debt. An individual can guarantee the debt of another individual or entity.

Can you refinance a house in an irrevocable trust?

Refinancing a house in an irrevocable trust is possible but only from irrevocable trust loan lenders. Conventional lenders cannot refinance a house in an irrevocable trust as the borrower is not currently on title of the property. The irrevocable trust loan lender can provide a short-term refinance loan that allows a beneficiary to buy out other siblings and then transfer the property into the beneficiary’s name. Once the property title is in the name of the new owner (an individual), the house can be refinanced into a long-term conventional loan.

Can a trustee borrow money from an irrevocable trust?

A trustee can borrow against real estate assets owned by an irrevocable trust as long as the original trust documents allow for borrowing against real estate. The trustee can borrow as long as the funds are used in the best interest of the trust and it’s beneficiaries.

Can a trust get a mortgage?

A trust can get a mortgage from a conventional lender while it is a living or revocable trust. Once the original trustees pass, the trust becomes an irrevocable trust and will only be able to receive short-term financing (1-2 years) from an irrevocable trust loan lender. Read more: Can a trust get a mortgage?

Can an irrevocable trust get a mortgage?

An irrevocable trust can get a mortgage secured by trust-owned real estate. The trust documents must allow for taking out a mortgage against the real estate by the successor trustee(s). The real estate owned by the irrevocable trust must also have sufficient equity in order to obtain a mortgage. Mortgage loans to irrevocable trusts must be approved by the successor trustee.

Can you use an irrevocable trust as collateral?

An irrevocable trust can use real estate assets as collateral to obtain a mortgage. Using real estate as collateral is typically the most cost-effective way to borrow against a trust’s assets. Read more: Using a trust as collateral for a loan

Can an irrevocable trust get a home equity loan?

An irrevocable trust can obtain a home equity loan against trust-owned real estate from a specialized trust loan lender. The real estate must contain sufficient equity relative to the loan amount being requested.

Can an irrevocable trust get a HELOC?

An irrevocable trust can obtain a loan against trust-owned real estate but typically not a HELOC (home equity line of credit). HELOCs are generally provided by conventional lenders for primary residences. Conventional lenders do not provide loans against real estate owned by an irrevocable trust.

Probate & Trust Loans Resource Guide

Jeff can be reached at 760-722-2991 or jeff@northcoastfinancialinc.com

California Irrevocable Trust Loan Request

We will contact you to review the loan scenario and provide a quote.